We are not "bound" by our budget in the sense that we never do anything fun. Our budget is more of a guide to show us where we spend our money and how much to put aside for certain expenses. Over the course of 5 years, our budget has constantly changed. Income has changed along with certain needs.

I'm not going to get very detailed (because there are honestly things that I still can't wrap my head around). Numbers and excel spreadsheets make my eyes cross. But I know how to control the money that I'm in charge of and I consider that my other full time job.

Basically here are the steps that we use:

1. Get our paychecks (I get paid at the end of the month) and Josh gets paid twice a month, and figure up the income.

2. Set up the excel spread sheet for what needs to go where. Mortgage, truck, and student loans get paid before anything else. For items we don't have exact amounts for we always round up (water bill, power, etc). Since he has kept everything so organized, we can look back to last year's (and really the last 4 years) "March" budget and see how much money we spent. That guides us and we usually have some left over.

3. Set aside money for car tags and our home loan (we bought in 2008 and there was an $8,000 bonus we were "given" that has to be paid back over the next 15 years). We put this aside each month so at tax season (if we owe) we have it. The past 4 years we haven't owed, so that money has just built up.

4. I figure out how much I have for groceries and the other budgets I am responsible for. We set aside $360 a month for groceries, toiletries, home stuff (dish soap, etc), and eating out. This will go up to $450 when the baby comes to cover formula and other baby things that we need. We found Luke cost us an extra $90+ a month. He was in disposables, so we're hoping that we won't have to use all that we will budget. I also keep up with dog expenses, kids (clothes, shoes), my budget (hair cuts), and thrifting/decorating. All that gets rolled together and it equals about $160 per month.

5. Make sure what we earn isn't less than what we are spending!

5. Make sure what we earn isn't less than what we are spending!

How do I keep up with everything?

I started by using the envelope system with cash. I liked it and it helped me remember that once the cash is gone, it's gone.

{source}

After about a year of "training" myself, I decided to switch back to our credit card. Although this is a cardinal sin for some, I will add that we currently have no credit card debt. We pay off our balance at the end of the month. And the rewards/points/moneyback we get from using our credit card can't be beat. So that's why we switched.

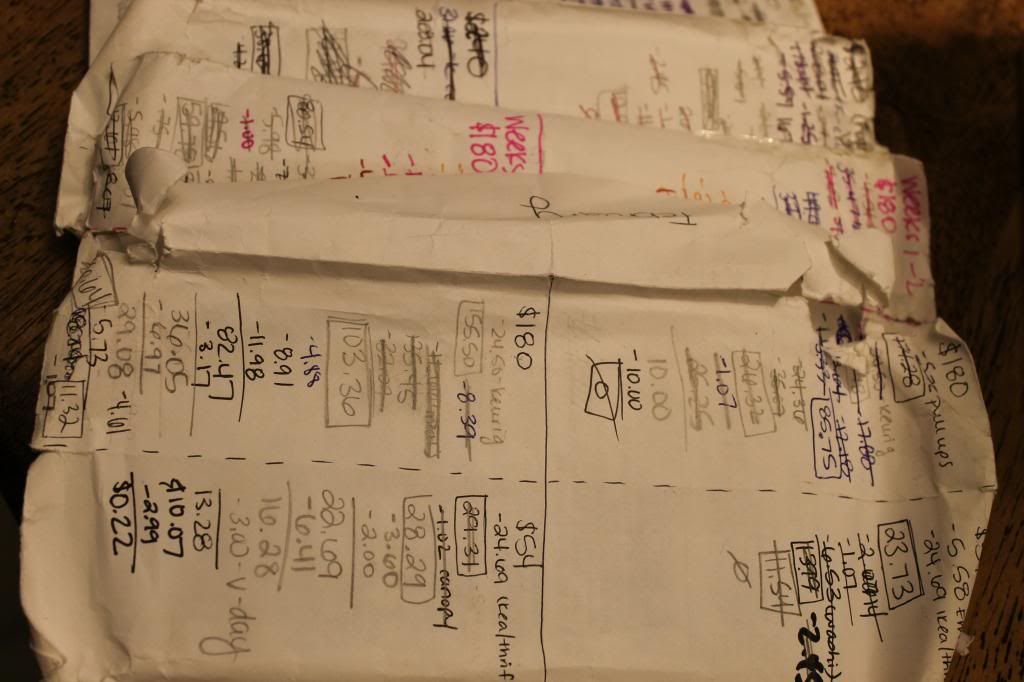

Even with using credit cards, I still have to keep up with purchases. Here's another type of "envelope" system I found on pinterest. It made so much sense for our needs that I decided to give it a try. Here's a picture of last month's envelope:

Yes, it gets messy and the envelope is ready for retirement after the month. It lives in my wallet the.whole.month. But it gets the job done. The best part? All the receipts go inside the envelope and if I ever had to go back and find one, then they are all there.

Basically I have split the envelope into 4 quarters. The column on the left are food (top quarter is the first 2 weeks, bottom quarter is the 3-4 weeks). That's where I budget the $360 (broken down to $180 for weeks 1-2 and 3-4. The column on the right is for the $160 other things (dog, kids, me). It's broken in half to spread out over the 2 week spans. I keep up with purchases much like the register of a checkbook. Sometimes I'll subtract what I spent right there at the register; other times I'll put all my receipts in once place and do it once I get home.

There really was no particular reason I went with 2 week periods other than I got very overwhelmed planning for the month. I can meal plan for a month; but actually keeping up with the $$ was really hard. I found that I would spend most of the food budget in the first 2 weeks and then be scrambling by the end of the month. If I did it by the week, it didn't allow me to stock up if I found a great sale by using coupons. The 2 week plan seems to be my glass slipper.

I typically go on a huge couponing trip out of town at the beginning of the month. I'll hit Target, Sams (every other month), Publix, and Aldi. I'll add up how much I spent at each place and divide it over the month. So if the total spend was $120, I'll take out $60 from the first 2 weeks and $60 from that last 2 weeks. That way I'm still on track with the weekly things I need to get from the grocery store and that huge trip doesn't wipe out my weeks 1-2 budget.

Sams gets tricky because some things last us for MONTHS. I typically know which items will last us and sometimes I'll roll it over to the next month. This is the ONLY time I'll do that. It's dangerous to "spend money before you make it". A perfect example is rice. I'll buy a huge bag of rice and know that it'll last me 3 months. So I'll refill our rice container (and put the rest out of reach). I'll leave myself a note on the back of my envelope to take the $$ out of the next 2 months. And when the next 2 months come I'll refill my rice container and I'll deduct it from those months.

I still coupon on top of all of this. It sounds overwhelming, but after doing it for over 2 years it just becomes second nature. I found with the cash envelope system I was hoping to have cash left over at the end of the month to roll over and "save" for the next month. But for me cash was just too easy to spend.

The last 2 months with my new credit card envelope system I have had money left over at the end of the month that gets absorbed into our bank account. It's like instantly adding money to our savings account.

Ironically, the last 2 months I have kept myself out of Walmart. I decided at the beginning of January to no longer go (these are personal bad experiences reasons). It's amazing how "I've survived"! I do have to be more strategic with making sure to grab what we need at the beginning of the month. But honestly with my coupon stockpile, we pretty much have plenty (deodorant, shampoo, etc). Also, we ran out of our ink cartridge last month. I jumped on amazon (we have prime) and ordered one and it was at my door in 2 days. Nothing HAD to be printed in those 2 days, so we waited. I may have spent $1-$2 more, but that's ALL I BOUGHT. Had I gone in Walmart I probably would have spent $20+ by seeing things I "need". Also Walmart made it "sew" easy to grab my sewing supplies (thread, fabric, etc). Now I just keep my eyes open for sales through hobby lobby and joanns and order what I need when they run free shipping sales. Or I will run in there when I do my huge trip at the beginning of the month.

I still grocery shop about once a week for fresh produce, dairy, etc. I don't like the stress of getting EVERYTHING at the beginning of the month. But these trips tend to run me less than $30 (some weeks it's less than $10). It just depends on the meals we are having that week/what is going on.

I must say that as "rigid" as a budget sounds, it has actually allowed us to do more. We KNOW when we have extra money and we know when we don't We know exactly where we stand with our finances. And we have a plan for paying off our debt. If we tackle these in small steps, we will eventually get through it! As of today we will have our roof paid off in June, the truck in Aug-Sept, and student loans soon after. It feels great to be getting somewhere!!

Sorry this post had so many words and so few pictures! I always enjoy reading how others budget/organize their life so I thought I'd put it out there!

No comments :

Post a Comment